A-Z of internal banking fraud

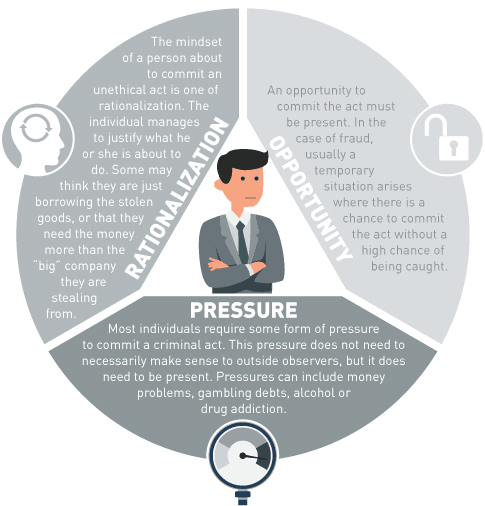

IT IS NO EXAGGERATION TO SAY THAT THE GREATEST FRAUD RISK THAT BANKS FACE WALKS THROUGH THEIR DOORS EVERY MORNING AND SITS DOWN TO WORK

Frauds carried out by bank employees are a huge global problem. In its 2022 Report to the Nations, the Association of Certified Fraud Examiners (ACFE) assessed 2,110 cases of internal fraud from 133 countries, which led to estimated losses of $3.6bn.

The A-Z of Internal Banking Fraud highlights the scale of this problem and the different vulnerabilities that internal fraudsters exploit, and explains how advanced anti-fraud technologies can combat it. Bank employees are uniquely well placed to discover and take advantage of weaknesses in their organization’s internal controls – perhaps by abusing their level of access to the bank’s IT systems or by targeting dormant accounts.

But FinTech anti-fraud solutions are improving all the time – their ability to identify and block suspicious activity in real time is becoming the first line of defense against the biggest fraud risk in banking.

Transaction reversal by tellers

Transaction reversal by tellers Account manipulation

Account manipulation Loan applications

Loan applications Hiding losses

Hiding losses Internal collusion

Internal collusion Data theft

Data theft IT changes at the back end

IT changes at the back end